The private credit market has rapidly grown and significantly reshaped the financial landscape today. Corporate lending traditionally has been the arena of banks and public debt markets, but it has come to be dominated by private credit providers, such as direct lending funds, private debt funds, institutional investors and alternative asset managers. This presents a new challenge for the banks as they are now facing the challenge of effectively integrating the private credit exposure within their wider risk management and compliance framework.

Private credit has gained popularity due to the flexibility in financing options it offers the borrower, and the possibility of higher returns for the lender. This is not without certain risks, however, such as decreased transparency, less liquidity, intricate deal structures and increased regulatory scrutiny.

Private credit risk can cause regulatory fines, higher capital requirements, credit losses, damage to a bank’s reputation and disruption of operations if not managed properly. Thus the adoption of private credit risk management to a company’s compliance program is no longer a choice but an imperative.

This article delves into the construction of a solid bank compliance framework for private credit risk integration that secures compliance with regulations, robustness of the organization and sustainable growth.

Understanding Private Credit and Its Risk Landscape

What Is Private Credit?

Private credit is financing which takes the form of debt that is provided by non-public lending institutions that do not participate in the public bond market. These loans typically are negotiated and tailored to the individual borrower’s needs, and are made privately.

Examples of private credit products are:

• Direct lending

• Mezzanine financing

• Unitranche loans

• Asset-based lending

• Distressed debt

• Special situation financing

• Infrastructure debt

• Real estate debt

While private credit is often a hallmark of alternative investments firms, banks are also getting involved into the sector in a variety of ways, including co-investment, acquisition, partnerships, and portfolio exposure.

Why Private Credit Is Growing

The expansion of private credit has been spurred by a number of factors:

Regulatory Changes

The traditional banks’ capital requirements were raised after the financial crisis, allowing the private banks to grow.

Demand for Flexible Financing

Many purchasers are looking for specialized loan services which might be obtainable in the conventional banking institution.

Investor Search for Yield

The institutional investor buyers are still looking for higher returns in different interest rate scenarios.

Market Inefficiencies

Private credit providers are likely to fill the pockets of market segments which haven’t been served by traditional credit providers.

With the growth of private credit, banks need to adapt their risk oversight framework.

The following four categories are considered to be the key ones to watch in Private Credit:

Credit risk continues to be the greatest risk.

Potential concerns include:

• Borrower default

• Weak cash flows

• Excessive leverage

• Poor management quality

• Deteriorating business conditions

Assessing creditworthiness can be more difficult than evaluating firms that are publicly traded, because there is less information that is publicly disclosed about private credit borrowers.

Concentration Risk

Excessive exposures can be built up in banks without their knowledge to:

• Specific industries

• Geographic regions

• Economic sectors

• Financial sponsors

• Individual borrowers

A high concentration makes people more prone to be vulnerable during economic downturns.

Liquidity Risk

Often private credit investments are not as liquid as publicly traded securities.

Risks include:

• Limited secondary markets

• Longer exit timelines

Issues related to getting a fair valuation.

When stressed, decreased flexibility

Operational Risk

There are various reasons for operational failures, such as:

• Inadequate due diligence

• Weak internal controls

• Data management failures

• Documentation errors

• Technology breakdowns

The more complex the bigger the portfolio.

Regulatory Risk

Private credit markets remain a focus of financial regulators’ attention.

Some possible non-conformance issues are:

• Inadequate reporting

• AML deficiencies

• KYC violations

• Capital adequacy issues

• Governance weaknesses

The Need for Private Credit Risk Integration

Many banks have traditionally exposed themselves to private credit, apart from their loan book. This piecemeal approach could also lead to partial risk assessments and monitoring.

An integrated framework provides:

Enterprise-Wide Visibility

There is a single overview of risk for the senior management.

Consistent Risk Assessment

The use of standard methodologies is beneficial for decision making.

Better Regulatory Alignment

Integrated controls help to streamline reporting requirements for compliance.

Enhanced Portfolio Monitoring

Early warning indicators are more effective if they are used on a consistent basis.

Improved Capital Planning

Risk measurements are an accurate indicator of risk which aids in the allocation of capital.

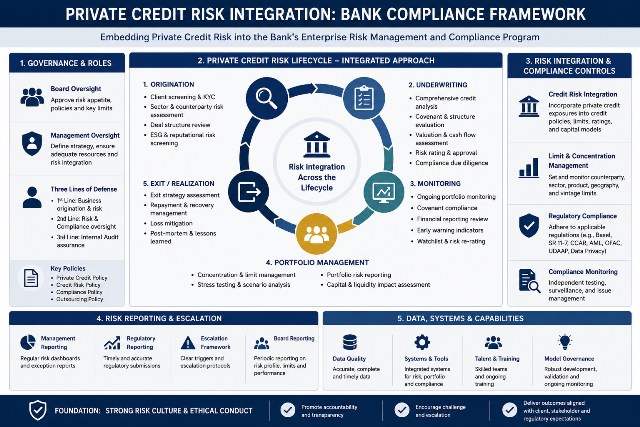

Core Components of a Bank Compliance Framework

Governance and Oversight

The essence of good governance is the basis of effective risk management.

Board Responsibilities

The board should:

• Define risk appetite

• Approve policies

• Monitor risk exposure

• Review compliance performance

• Ensure accountability

Risk Committees

To ensure continuity of the oversight, risk committees do so through:

• Portfolio reviews

• Escalation procedures

• Stress-testing assessments

• Policy evaluations

Senior Management

Management must ensure:

• Framework implementation

• Resource allocation

• Policy enforcement

• Continuous monitoring

Good governance permeates and instills good compliance within the organization.

Risk Appetite Framework

Banks should have a clearly defined criterion for acceptable levels of risk.

Key metrics include:

• Portfolio concentration limits

• Sector exposure thresholds

• Credit rating requirements

• Leverage restrictions

• Geographic diversification standards

A risk appetite statement provides guidance on decision making and helps to stop over- or under-risking.

Policies and Procedures

All policies are comprehensive, setting clear expectations.

Policies should address:

Credit Approval

The underwriting and approval requirements.

Due Diligence

Standards for borrower evaluation, and risk assessment.

Monitoring

Ongoing review requirements.

Reporting

The reporting of risks and reporting deadlines.

Escalation

Mechanism to deal with new issues that arise.

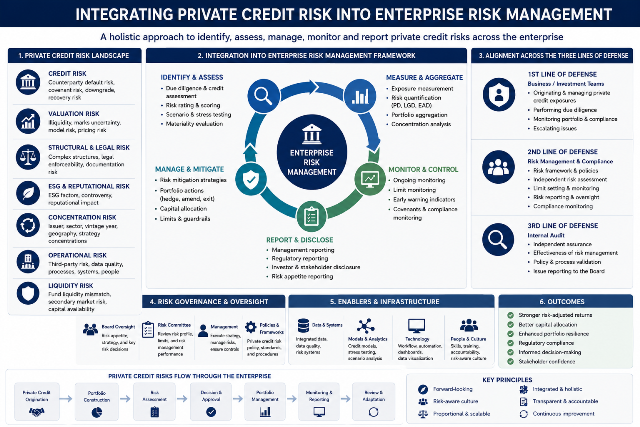

Integrating Private Credit Risk into Enterprise Risk Management

Risk Identification

Identification of risk should be done prior to, during and after the investment decision.

Some of the key areas of assessment are:

Borrower Analysis

Evaluate:

• Financial performance

• Cash flow stability

• Debt capacity

• Management quality

Industry Assessment

Consider:

• Market trends

• Competitive pressures

• Regulatory changes

• Economic conditions

Sponsor Evaluation

Assess:

• Track record

• Financial strength

• Governance practices

• Strategic objectives

Risk Measurement

There needs to be quantitative and qualitative measurements to measure the effectiveness of integration.

Common techniques include:

The likelihood that the borrower will fail to pay back a loan.

Measures the risk of the borrower defaulting.

Loss Given Default (LGD)

Calculate any losses that may occur if there is a default.

The amount of exposure a defaulting borrower has to the lender.

Computes exposure when there is default.

Expected Loss Models

Uses a combination of PD, LGD and EAD to estimate potential losses.

Risk Monitoring

The continuous monitoring assists to spot new dangers.

These important indicators of monitoring are:

• Covenant breaches

• Delayed payments

• Rating downgrades

• Financial deterioration

• Market disruptions

Automated monitoring systems can detect the issue quickly and accurately.

Also Read: Risk Management in Infrastructure Projects

Regulatory Compliance Considerations

Capital Adequacy

Banks need to have adequate capital to compensate for potential losses.

Private credit exposure are frequently exposed to increased capital planning because of:

• Illiquidity

• Complexity

• Valuation uncertainty

There should be stress scenarios and adverse economic factors included in the capital adequacy assessment.

Anti-Money Laundering (AML)

AML compliance continues to be one of the regulatory requirements.

Key controls include:

• Customer verification

• Transaction monitoring

• Suspicious activity reporting

• Enhanced due diligence

If AML standards are not met, there will be substantial penalties.

Customer Identification Program (CIP)

Implementing effective KYC programs assist banks to:

• Verify borrower identities

• Assess beneficial ownership

Identify, assess and monitor financial crime risks

• Meet regulatory obligations

An effective KYC is crucial on complex private credit deals, particularly.

Data Governance

High-quality data supports:

• Regulatory reporting

• Portfolio analysis

• Risk measurement

• Internal audits

Banks need to have a clear criterion on how data should be accurate, complete and consistent.

Stress Testing and Scenario Analysis

Stress Testing is important because…

A variety of economic downturns can be different in the behavior of a private credit portfolio.

A stress test measures a person’s resilience in the face of stress.

Examples include:

• Recession scenarios

• Interest rate shocks

• Industry-specific downturns

• Liquidity crises

Scenario Analysis

A list of events that could impact banks is provided and scenario analysis is used to gain understanding of how these events could impact:

• Default rates

• Recovery values

• Portfolio performance

• Capital requirements

Frequent testing is a way to increase preparedness and strategic planning.

Technology and Digital Risk Integration

Develop a Technology and Digital Risk Integration plan.

Risk Analytics Platforms

Today’s analytics solutions allow for:

• Portfolio surveillance

• Predictive modeling

• Concentration analysis

• Regulatory reporting

These applications help increase transparency of the large portfolio.

Artificial Intelligence and Machine Learning

Get to know Artificial Intelligence and Machine Learning.

AI solutions can help improve:

Credit Scoring

Improved borrower assessment.

Predictive Risk Monitoring

Early identification of poor credit.

Anomaly Detection

The identification of abnormal borrower behavior.

Compliance Monitoring

A computer-driven identification of violations of policies.

Automation

Automation helps to minimize human mistakes and boost productivity.

Applications include:

• Loan onboarding

• Documentation reviews

• Regulatory reporting

• Covenant monitoring

How to achieve successful Private Credit Risk integration – Best Practices.

Establish Cross-Functional Collaboration

The various departments need to coordinate, such as:

• Risk management

• Compliance

• Legal

• Finance

• Operations

• Business units

Standardize Methodologies

Consistent frameworks improve:

• Reporting quality

• Portfolio comparisons

• Regulatory transparency

Enhance Documentation

Documentation should support:

• Audit requirements

• Regulatory examinations

• Internal reviews

• Decision-making processes

Conduct Regular Reviews

Regular reviews will help to keep frameworks relevant to the evolving market and regulatory landscape.

Invest in Training

Staff should understand:

• Credit risk principles

• Compliance requirements

• Regulatory developments

• Technology tools

A knowledge and informed workforce adds to the overall risk culture.

Common Challenges

Banks frequently encounter:

Data Limitations

Less standardised information is typically available from private credit markets.

Resource Constraints

It is often hard to find knowledgeable, skilled personnel.

Regulatory Uncertainty

The expectations for supervisors are constantly changing.

Complex Structures

There may be a need for additional supervision when handling customized transactions.

Valuation Difficulties

It can be difficult to know exactly how much value is in a company’s illiquid assets.

The challenges need to be addressed proactively through good governance.

Private Credit Risk Management – Trends for the future

There are likely to be a few developments that will impact the future:

• Increased regulatory oversight

• Enhanced transparency requirements

• Greater AI adoption

• Real-time risk monitoring

• Improved data analytics

• Stronger governance expectations

The management of risk has been an integrated element of enterprise risk platforms.

The banks with the progressive outlook will have the advantage in dealing with the new risks arising.

Key Takeaways

Private credit is still growing in financial markets at a very fast pace.

Private credit risk needs to be incorporated in the enterprise compliance structure of banks.

The governance, risk measurement and monitoring are key.

Compliance with the regulatory requirements continues to be a critical issue.

Technology can be a very effective tool to enhance risk oversight.

Stress testing increases the resilience and preparedness.

Documentation and training are strong and result in long-lasting success.

Frequently Asked Questions

Private credit risk is the risk associated with a company’s debt.

Private credit risk is the risk of a loss due to private contracts for credit.

What is the significance of private credit for the banks?

It offers loan options, diversification of investment portfolios, and also prospective income growth.

What do you consider to be the biggest risk in private credit?

The default risk of the borrowers is usually the dominant concern, as it relates to credit risk.

In what ways does compliance aid in risk management?

Compliance is defined as when activities are in line with the rules and policies, as well as what is expected.

What is the value of governance?

Governance fosters accountability, transparency and effective governance.

What are the advantages of using technology for integrating risk?

The use of technology improves monitoring, reporting, analytics, and decision making.

What is the part of stress testing?

Stress testing is a method of assessing the ability of a portfolio to withstand negative conditions.

How often should the private credit portfolio be reviewed?

Reviews are on-going and formal reviews are carried out regularly.

What are some likely regulatory concerns?

AML (Anti Money Laundering), KYC (Know Your Customer), capital adequacy, reporting accuracy and governance effectiveness.

So what’s in store for private credit risk management?

Future holds promise of greater automation, advanced analytics, AI use and regulation.

Conclusion

Private credit has emerged as a big part of the financial markets today, and presents both new prospects and new dangers for banks. The growing exposure to private lending should not be ignored, as institutions need to make sure their risk management and compliance structures are able to adapt to this. To ensure effective private credit risk integration, proper governance, well-developed risk assessment practices, ongoing risk monitoring, regulatory fit and advanced technology solutions are essential.

Those banks that are able to incorporate private credit risk within enterprise-wide compliance structures will gain better visibility, increased resilience, regulatory compliance and better decision making. With the financial landscape growing more and more intricate, risk integration going proactively is crucial for sustainable growth and long-term stability.